The approval of the Climate Disclosure Rule by the United States Securities and Exchange Commission (SEC) marks a significant milestone toward creating a more sustainable future. The rule requires publicly traded companies to disclose detailed information about their climate-related risks and Scope 1 and 2 greenhouse gas (GHG) emissions (if material) in their annual reports and registration statements. Many publicly traded companies were already disclosing this information. However, the disclosures were not always standardized and appeared in different formats, ranging from sustainability reports to company websites. This made it challenging for investors looking to fully assess their risks and opportunities. In contrast to the SEC’s approach, both Europe’s Corporate Sustainability Reporting Directive (CSRD) and California’s Climate-Related Financial Risk Act (SB 261) require private companies to report on their climate-related risks.

By requiring publicly traded companies to disclose detailed information about their climate-related risks and GHG emissions, the SEC is promoting transparency in the business community. While this is important, the rule has missed the opportunity to engage the millions of private companies that sit in the value chains of publicly traded companies. Due to the removal of the requirement to disclose value chain emissions (Scope 3), private companies are no longer directly in scope for reporting.

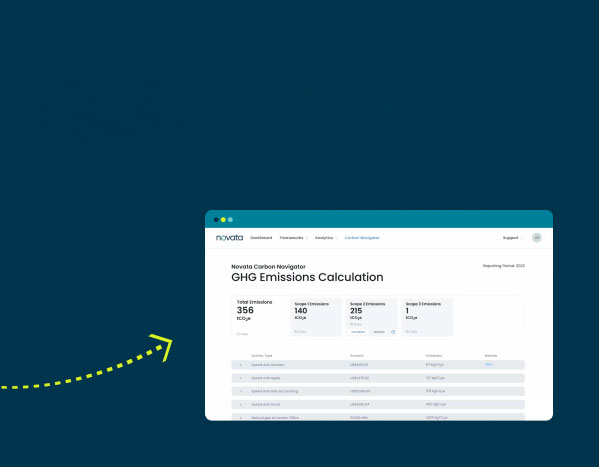

Scope 3 emissions represent the largest percentage of emissions for most companies. Typically, public corporations deploy strategies and personnel to engage their suppliers, including private companies, which make up part of their Scope 3. Excluding this information from the standardized disclosure leveraged by investors in the capital markets means no one is getting the full picture of the risks facing large companies and their private company partners.

A recent study by Parchomovsky and Eckstein published by the University of Pennsylvania Carey Law School found that there is no significant gap in governance between the largest 200 public companies and private companies. One of the reasons for this is that private companies adopt the norms of the business environment in which they operate. On a voluntary basis, investors in private companies have been adding climate-related metrics to their models. The data is collected and used across the lifecycle of an investment. Beyond this, industry alliances and stakeholder initiatives are adding climate-related metrics to their disclosure recommendations.

Private companies just getting started with climate reporting will find that adopting new practices, enhancing data collection and reporting infrastructure, and integrating climate-related measures into risk assessments and decision-making will require cross-functional work. New players will need to engage. This includes a company’s CFO, audit committee, assurance providers, and others, who will all need to come up with the learning curve and closely review climate-related and GHG metrics.

By refining climate governance, companies will upskill their boards, management, employees, and other stakeholders. They will also invest in existing systems capabilities, review historical data, and set processes leading up to the limited assurance required for filers. Understanding gaps in policies, processes, and control is key.

Whether or not they are mandated, climate-related disclosures are crucial for businesses to identify and tap into opportunities to create long-term value, which leads to stronger and more financially resilient companies. Novata can help companies get an accurate picture of their climate-related risks and GHG emissions, no matter where they are in their journey. To learn more, take a look at Novata’s carbon management page.